|

Understanding Money |

In this section we break down a number of points into bite-sized pieces. You can find them recreated on a single page here.

1. How Money Really Works

An Example

In order to show how money really works, we can offer a simple example. We'll build a small financial system that shows how communities create and use money, and how things like banks and debts really work too.

We'll keep it very simple. We'll start with a very small community, a community of just 5 people, who have skills they want to trade among themselves, in what we could call a 'local economy'. We'll show how they can interact with each other using money and doing so will capture how we interact with each other in much larger societies, indeed the world as a whole, today.

2. Conceptualizing Money

The Fountain of Money at the Heart of All Economics

This one is just a little conceptual aid, for those who might benefit from it. I think it can help to make sense of economic reality and aid in breaking down some unhelpful economic myths.

This one is just a little conceptual aid, for those who might benefit from it. I think it can help to make sense of economic reality and aid in breaking down some unhelpful economic myths.

I'm sure you've heard people say "Money doesn't grow on trees!" "There's no such thing as a magic money tree!" etc. But the fact is that all money has to be created and we create it through processes which make money creation as simple and inexpensive as possible. You could think of these processes as magic money trees, but I prefer to think of them as fountains of money that exist at the heart of all our economies. And they've really always been there.

3. Public Money Creation

Breaking it Down

We've said that two of the most elementary observations that can be made in the field of monetary economics are:

- Every country should have a debt-and-interest-free national currency base.

- All households and all governments should have access to interest free financing.

And that's because money is created in two spheres:

4. Physical Money

Nothing More Than a Communications Device

Physical notes and coins exist in the smallest number possible to facilitate day to day trades, to convey accounts information outside the banks' secure networks. In other words, they are simply durable, reasonably secure communications devices, carrying accounts information, hand-to-hand, across the economy. The materials of which modern money is made have no intrinsic value, you could not get anything for the paper or base metals out of which they are made. But neither are they supposed to, because they only exist to carry information. You could liken money to any other legal agreement that might be recorded on paper; the paper on which a contract is signed has no intrinsic value, its value lies in the information or agreement it memorializes.

Physical notes and coins exist in the smallest number possible to facilitate day to day trades, to convey accounts information outside the banks' secure networks. In other words, they are simply durable, reasonably secure communications devices, carrying accounts information, hand-to-hand, across the economy. The materials of which modern money is made have no intrinsic value, you could not get anything for the paper or base metals out of which they are made. But neither are they supposed to, because they only exist to carry information. You could liken money to any other legal agreement that might be recorded on paper; the paper on which a contract is signed has no intrinsic value, its value lies in the information or agreement it memorializes.

5. Banks as Credit Agents

For Households and Nation States

This is just a brief look at how the relationship between the financial sector and individuals or their governments should properly be. Inherently, it involves a consideration of the deep and far-reaching conflict between money as a tool for socioeconomic progress and money as a tool for often ruthless domination and extraction.

6. It's Just Not Scientific

The World's Most Powerfully Misused Words

The words 'lend' and 'borrow' already have their use and meaning in the world outside of finance. Say I have a bicycle and you would like to 'borrow' and make use of it for a period before returning it to me, I could 'lend' that bicycle to you and the interaction between us really would be an example of what our language ordinarily conveys by the words 'lending' and 'borrowing'.

The words 'lend' and 'borrow' already have their use and meaning in the world outside of finance. Say I have a bicycle and you would like to 'borrow' and make use of it for a period before returning it to me, I could 'lend' that bicycle to you and the interaction between us really would be an example of what our language ordinarily conveys by the words 'lending' and 'borrowing'.

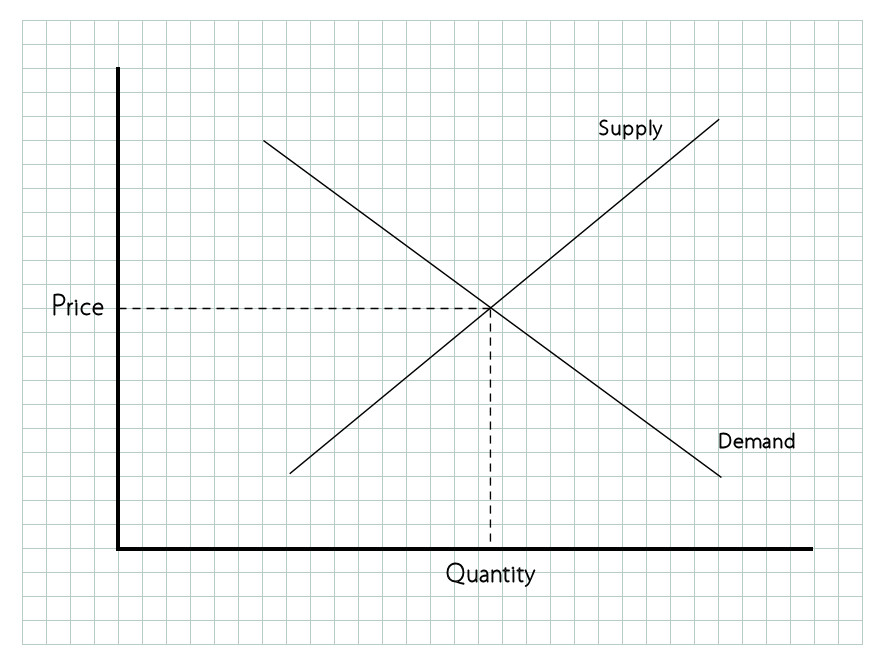

7. Capitalism

The Basic Economics

- Fig 1 -

In our earliest studies of economics, we're introduced to the idea of supply and demand (click the pictures to enlarge them). And despite the many complications this simple analysis can gloss over, I think it can be an important thinking tool nonetheless.

8. Accounting for Money Creation - 1

Introducing Governments and Banks

We've seen how money, banking and debt, in truth, basically work and we've considered a few conceptual ideas to strengthen our understanding of what is going on, what is going wrong and how we might fix it.

9. Accounting for Money Creation - 2

Introducing a Plurality of Banks

In the previous section, I built on our earliest look at how money really works and established that we could continue to develop that example economy, to include a government and formal banking, and retain a form that was democratically legitimate and fair, that did not subjugate the community to class hierarchical relations and systemic usury.

next |